Mixed Results in June; Tech Stocks Continue to Outperform

The equity market hit a year-to-date high in June but was tempered by emerging coronavirus cases as states slackened their isolation orders, ending with a near flat month after three months of sustained rebound from the March 23 low.

The COVID-19 pandemic continues to drive fiscal and monetary policy, and as Federal Reserve Chairman Jerome Powell has said he expects the central bank to continue its support, Congress may soon start negotiating another round of fiscal stimulus.

As the results of loosening restrictions play out, investors should expect some volatility as new cases arise and states respond by pausing or stepping back their phased approaches.

Currently, the state of the equity markets appears to be in two parts: tech and everyone else. Much of the growth of the equity market has been on the strength of technology stocks, which continue to see gains where other industries have experienced downward pressure and disruption to their markets. We thought we’d share a high-level summary for now, but you can always read the full market letter for more details on the latest economic data and U.S.-China relations and how they may be impacted by the presidential election.

- June marks the first month since March where equity markets haven’t closed meaningfully higher than where they opened. As states ended lockdown restrictions, a rapid increase in COVID-19 cases weighed on stocks as phased reopening plans have been paused or called into question in some areas.

- Continued support from monetary policymakers and a new round of fiscal stimulus could continue to blunt the worst economic effects of the pandemic.

- Volatility should be expected in the coming months as states emerge from lockdown, and then pause or step-back phases of their reopening plans.

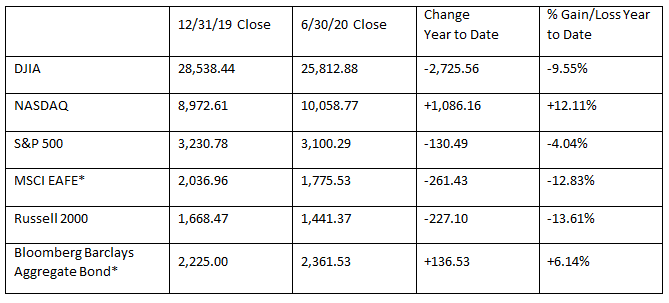

Performance reflects price returns as of market close on June 30, 2020. EAFE and Bloomberg Barclays Aggregate Bond performance reflects June 29 closing values.

Bottom line

The coronavirus numbers are troubling, but continued fiscal and monetary support are expected to blunt the worst of the economic effects of the pandemic.

Expect volatility in coming months as states phase out their lockdown restrictions and will likely continue to face rising infection rates. However, improving treatments and continued vaccine development remain promising.

“It makes logical sense for the market to slow down or pause in the short term following such enormous strength off the March 23 lows,” Madere said. “Importantly though, historical performance following similar surges out of recessionary bear markets has been very favorable over the next 12 months. This contributes to our positive bias and view that pullbacks should be used as buying opportunities.”

As always, if you have any questions – about the markets, your financial plan or anything else – please reach out to us. Thank you for your continued trust.